ESPP: Adjust Cost Basis to Avoid Double Taxes (Morgan Stanley, Workday)

I think examples are easiest to work with so let’s go with a simple one. Here’s some information about your company (ABC)’s ESPP :

- ABC gives 15% discount on the stock on the last day of the quarter

Why do I need to adjust your cost basis or change anything on my tax forms?

Technically, you don’t, but if you don’t adjust the cost basis for the capital gains that you get on your 1099-B for ESPP if you have a disqualifying disposition, you will be double taxed on the ESPP that ABC gives you at a discount (15%).

Why would I be double taxed?

Because circa 2014, there was a law change about how the cost basis for ESPP should be recognized. As a result, the 1099-B only includes information about what the purchase price was for you, not the purchase price it was without the “discount” on the stock (at ABC, that is 15%). We don’t want that “discount” to show up on the 1099-B because it already shows up on your W-2.

Is it adjusting cost basis “hard”?

While the below information goes into a lot of detail to explain how the double taxation is happening, finding the cost basis and adjusting that number itself is not hard if you don’t do a lot of trading in your account and know where to go to for the cost basis. All you need is 4 numbers/cost basis (1 for each quarter assuming you are enrolled in ESPP the entire year) and adjusting it in your tax software is typically a few clicks and entering in the number. Below documents the various ways you can obtain the cost basis.

Understanding how ESPP works: Example

Go here for another explanation: https://turbotax.intuit.com/tax-tips/investments-and-taxes/employee-stock-purchase-plans/L8NgMFpFX

With easy numbers, let’s pretend:

- ABC stock was $100 market price

- ABC stock granted to you was 15% off at $85 (aka you purchased it at $85. This is your cost basis)

If you sell your stock right away at $100, the price you got it for, you “should” be taxed on:

- W2 should have the $15 (15%) discount of your ESPP because this was a work benefit in the same way your Health & Wellness Benefit appears

- 1099-B should have $100 cost basis because that’s technically the price it was worth and then if there is a gain/loss from here, it would appear as short term capital gains.

It used to clearly indicate that on your 1099-B so you can edit your cost basis, but circa 2014, it no longer did.

NOW:

- W2 should have the $15 (15%) discount of your ESPP (still does)

- 1099-B should have $85 cost basis (this means you are double taxed on the $15 you get off)

This means:

- You will be taxed on $15 on your W2 because it is included in your income

- You will be taxed on $15 on your 1099-B because officially, you would have sold for $100 and cost basis is $85.

- In total, you will be taxed on the $15 in two separate tax forms. In order to be not be taxed on two forms, we kind of “edit” one of them which ends up on Form 8949 on your tax return.

Understanding how ESPP works: Technical Terminology

Let’s break down what happens when you have ESPP:

- ESPP gives you a discount on a stock → that is some sort of “disposition”, this is actually called “bargain element” but in any case, it’s basically free $ that you get from the company

- But whenever you have a stock, you get taxed on losses/gains → that becomes short OR long term capital gains

When you sell the ESPP, determines whether or not #1 becomes a qualifying or disqualifying disposition.

These are basically all the options you can come across for ESPP:

Option 1: Disqualifying disposition + Short Term Gain/Loss

- Qualification: Sell shares < one year from purchase date

- Bargain Element (your 15% discounted) is treated as: Ordinary income (it appears on your W2) which is Short Term Rate

- Gain/Loss is treated as: Short Term Capital Gain/Loss

Option 2: Disqualifying disposition + Long Term Gain/Loss

- Qualification: Term Gain/LossSell shares at least one year from purchase date but not two years from the offering date

- Bargain Element (your 15% discounted) is treated as: Ordinary income (it appears on your W2) which is Short Term Rate

- Gain/Loss is treated as: Long Term Gain/Loss

Option 3: Qualifying disposition + Long Term Gain/Loss

- Qualification: Sell shares at least one year from the purchase date and at least two years from the offering date

- Bargain Element (your 15% discounted) is treated as: Long Term Gain (it DOES NOT appear on your W2)

- Gain/Loss is treated as: Long Term Gain/Loss

How do I know if I have a Disqualifying Disposition?

The easiest way is to check your very last pay stub of that year, if it says Disqualifying Disposition → then you have a disqualifying disposition.

Unfortunately, it doesn’t spell it out that you have a Disqualifying Disposition anywhere else. There are only hints to it in your Morgan Stanley account, paystub, etc.

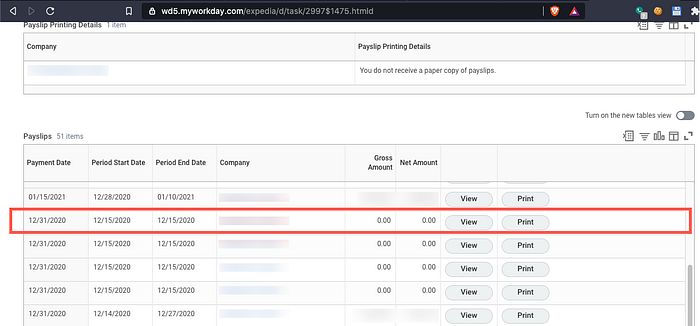

- Go to your last paystub of the year, this is the one for 2020. (Note: See how there are a few with the same dates in Workday? Well, not sure what that’s all about but my guess is that whoever is putting in the numbers are adjusting it)

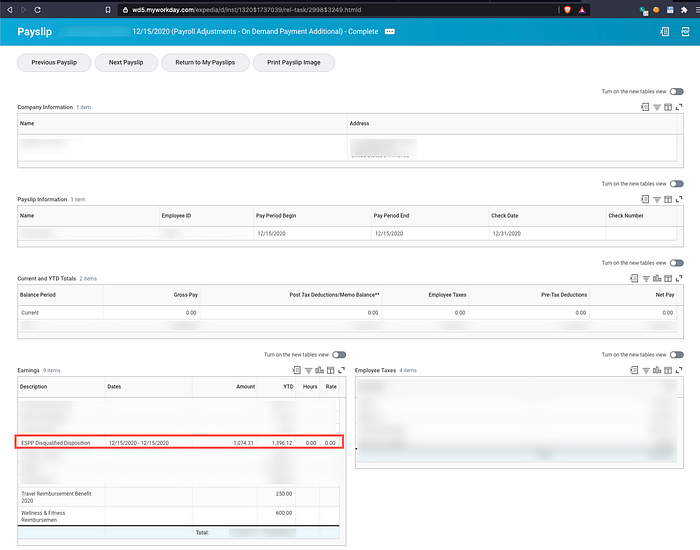

- Observe how your paystub notes “ESPP Disqualified Disposition” (Note: this does not show up as a separate box on your W-2. This is just included in the boxes 1, 3, 5) without any other distinction from anything else that appears in your “Earnings” box on your paystub. Those same boxes 1, 3, 5 includes our travel & wellness reimbursements, salary, bonus, etc))

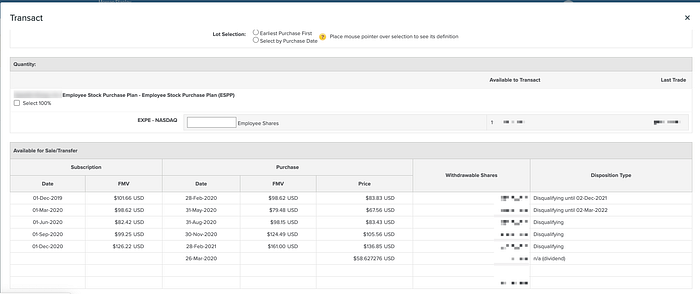

- Can figure out through Morgan Stanley if you act like you wan to Transact (sell) again. Go to: Dashboard > Employee Stock Purchase Plan > Transact > Transact (again)

Workday Payslip List

Workday Paystub

Morgan Stanley

So how do I determine what the cost basis is?

If you have determined that you have a disqualifying disposition and you need to adjust cost basis, it can be easier or slightly more more painful depending on whether you have always sold your stock as a single block or not. These are the tricks that have made it easier.

Option A: Use Form 3922

Note: This only works best if you always sold your stock as one “whole unit”, discretely based on when you purchased the ESPP. If you mix it, then this form is not exactly as helpful.

Option B: Use Morgan Stanley Events/Activity

Note: This works in all cases. This is especially helpful if you did not sell your stock as a “whole unit” upon each ESPP purchase. You will probably want to go this route if you see VARIOUS appear in your 1099-B.

Using Morgan Stanley Event (Easier if Date Acquired on 1099-B is VARIOUS)

- Gather your documentation (Morgan Stanley “Event”)

- Log onto https://stockplanconnect.morganstanley.com/

- Click on the “Activity” tab at the top

- You will land on the “Past Events” sub-tab

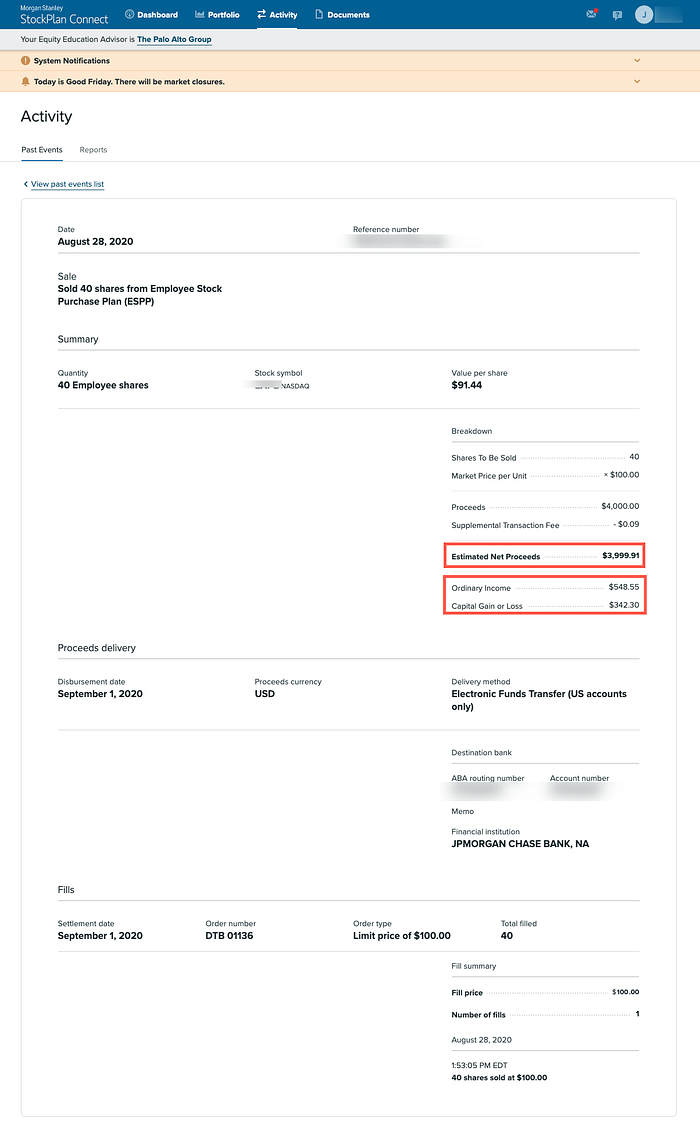

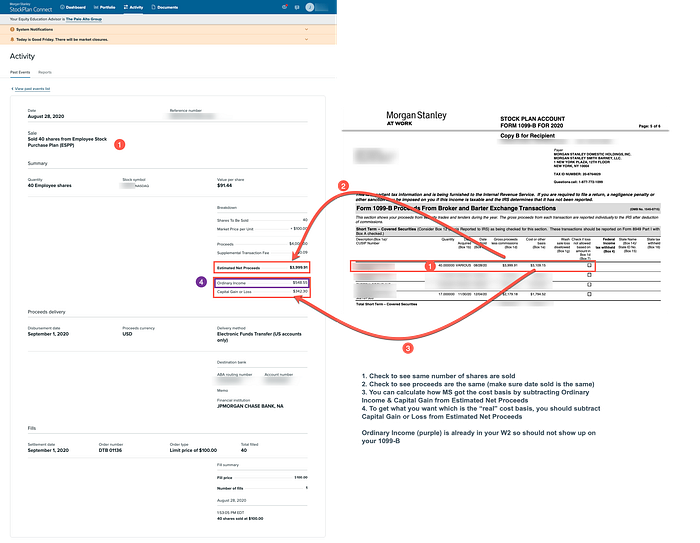

- Find the event when you sold, it should look something like this: Sold 40 shares from Employee Stock Purchase Plan (ESPP)

- Use the numbers here to fill out your cost basis by matching the total sales price

2. Construct a composite view of your forms:

- In the composite view: Make sure you have the right transaction

- Do the math: Estimated Net Proceeds — Capital Gain/Loss = Cost Basis that you adjust on your taxes

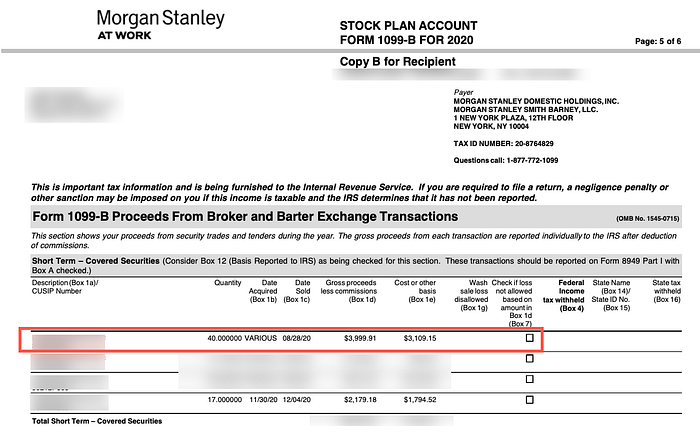

Morgan Stanley’s Event tells us:

- Estimated Net Proceeds: $3,999.91

- Ordinary Income: $548.55

- Capital Gain or Loss: $342.30

Morgan Stanley’s 1099-B tells us:

- Gross proceeds less commissions (Box 1d): $3,999.91 (see how it matches above)

- Cost or other basis (Box 1e): $3,109.15 ($3,999.91 — $548.55 — $342.30 = $3,109.15 from the above Event)

You should adjust so that $3,999.91 — $342.30 = $3,657.61

Once again: this is Estimated Net Proceeds — Capital Gain = Your Adjusted Cost Basis that you should enter to your taxes (get numbers from MS Events)

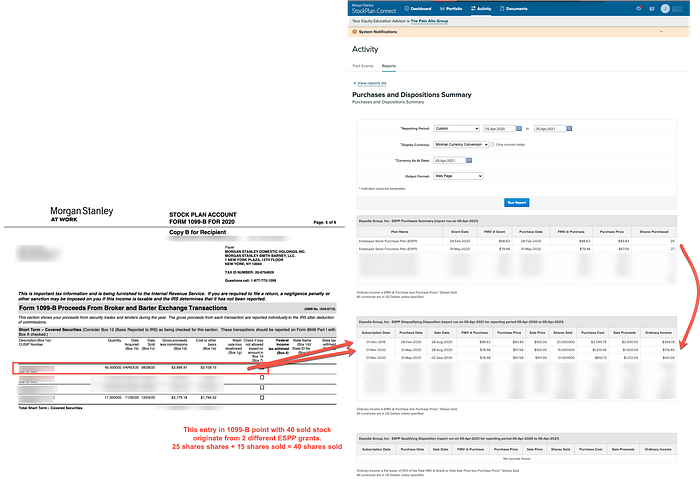

Using Morgan Stanley Reports/Purchase & Dispositions History

- Gather your documentation

- Log onto https://stockplanconnect.morganstanley.com/

- Click on the “Reports” tab at the top

- You can choose one or the other, if you choose Purchase & Dispositions Summary

- You can match up the corresponding amounts to your sale date

2. Multiply the “FMV @ Purchase” amount against number of shares (this will have to be done for each ESPP grant)

Morgan Stanley “Event”

Morgan Stanley 1099-B

Composite View

Morgan Stanley “Reports”

Option C. Estimated Method

Note: This works in all cases. This is especially helpful if you did not sell your stock as a “whole unit” upon each ESPP purchase. You will probably want to go this route if you see VARIOUS appear in your 1099-B. This may be slightly off, I would imagine by generally $1 at most. Given that often tax software often have a HALF_UP rounding, I’m not too worried about the IRS coming after me for some cents in discrepancy.

- Get your 1099-B

- Divide your Cost Basis by .85 (by dividing cost basis by .85, you are adding back in the 15% bargain element/ordinary income)

*Mental math double check in case you multiply instead of divide: This number should be higher than the Cost Basis listed on your 1099-B therefore reducing how much taxable income you have

- Based on previous section: The cost basis is $3,657.61

- Cost Basis from 1099-B: $3109.15

- Cost Basis from Estimated Approach: $3109.15/.85 = $3657.82

How do I do it on Turbo Tax?

See https://thefinancebuff.com/adjust-cost-basis-for-espp-sale-in-turbotax.html

How do I do it on HR Block?

See https://thefinancebuff.com/adjust-cost-basis-for-espp-sale-in-hr-block-software.html